Sign up for our monthly Leap Update newsletter and announcements from the Leap Ambassadors Community:

By clicking "Stay Connected" you agree to the Privacy Policy

By clicking "Stay Connected" you agree to the Privacy Policy

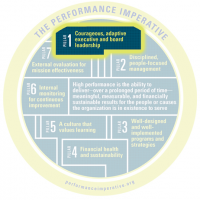

Our Common Definition of High Performance

Without a thoughtfully developed, thoroughly vetted definition of “high performance,” any call for raising performance in our sector rings hollow.

Definition

Courageous, Adaptive Executive and Board Leadership

Leadership, the preeminent pillar of high performance, helps your organization embark on a journey to make it even stronger.

Practice Imperative

Disciplined, People-Focused Management

Join forces to make your disciplined and people-focused management even stronger.

Practice Imperative

Well-Designed And Well-Implemented Programs And Strategies

Well-designed and well-implemented programs help the people and causes you serve.

Practice Imperative

Financial Health And Sustainability

Get on the path to long-term financial sustainability.

Practice Imperative

A Culture That Values Learning

Double down on developing a culture that values learning.

Practice Imperative

Internal Monitoring For Continuous Improvement

Internal data help you make decisions that leads to continuous improvement.

Practice Imperative

External Evaluation For Mission Effectiveness

External evaluation can help you ensure mission effectiveness.

Practice Imperative

A Community Bank Guide for Nonprofits

– Orv Kimbrough, CEO of Midwest Bank Centre

It’s no secret that nonprofits need access to capital to fulfill their missions.[1] Therefore, a relationship with a bank, especially one with a commitment to the organization’s mission and the communities they serve, can help you achieve that goal.

Orv Kimbrough, CEO of Midwest BankCentre and former CEO of the United Way of Greater St. Louis, has a renewed perspective about where nonprofits should place their money. He says, “Investing based on who’s contributing to my organization doesn’t necessarily translate into access to credit in the communities we purport to care about.” So, as a nonprofit, where do you invest your money?

Barbara Jessie-Black, President and CEO of CommunityWorx, a nonprofit with a business arm, says, “There’s a misunderstanding in some banking circles—that nonprofit organizations are too risky because our revenue is based on philanthropic giving and not necessarily earned income. That’s why the relationship with a bank is so important.”

Intentionally building a relationship with your community bank allows the bank to get to know your nonprofit organization and understand why you exist, how you operate, and your impact on the local community, which they also serve. Hilda Polanco, Managing Partner of BDO FMA, says “Build that relationship over time. It will serve you well when you need access to capital.”

The question about where nonprofits invest their money has become even more salient during the COVID-19 pandemic. Polanco says, “When the Paycheck Protection Program (PPP) launched, we learned that many community banks proactively reached out to nonprofit leaders to alert them about the PPP loan application. When a crisis hits, you want a solid relationship with a community bank. This connection will come in handy, especially in moments when things don’t go as planned.” If you don’t have a relationship with your community bank, how should you build it?

This guide aims to encourage nonprofits to be intentional about banking relationships. It includes insights from Leap Ambassadors and other social-sector leaders on what to look for in community banking relationships; specific, actionable steps organizations can take when considering a partnership with such institutions; and examples of community banks working in communities, particularly in under-invested communities. These recommendations aren’t exhaustive, as each nonprofit’s lifecycle, networks, capacity, mission, and zip code are different. These factors can play a part in a nonprofit’s ability to develop relationships with community banks.

Community banks are broadly defined and may include community development financial institutions (CDFIs), credit unions, minority-owned banks, and various types of retail banks such as a local branch of a national or multinational bank, a smaller bank with a regional or local presence, or an online bank. A community bank’s deposits should be insured by the Federal Deposit Insurance Corporation (FDIC).

Not all nonprofits have access to a local community bank. For example, if a nonprofit serves an under-invested neighborhood where there are no mainstream banks, that area is deemed a “banking desert.”[2] Hence, the organization might consider mission-driven financial institutions like one of the 143 minority-owned banks (or minority depository institutions).[3] Another option could be a CDFI, like the Local Initiatives Support Corporation (LISC), which has 38 local offices and rural programs in 45 states.[4] LISC connects local partners, including nonprofits, with hard-to-access public and private dollars to support underinvested places and people.[5] Yet another alternative could be an online banking institution. For example, Kimbrough’s Midwest BankCentre oversees the online bank, Rising Bank. Determining the type of community bank that meets your nonprofit’s needs is crucial.

Community Bank Definitions |

Type | Description |

Community Development Financial Institutions (CDFIs) | CDFIs measure success by focusing on the “double bottom line:” economic gains and their contributions to the local community. With community development as their mission, CDFIs supply the tools enabling economically disadvantaged individuals to become self-sufficient stakeholders in their own future.[6] There are CDFIs focused on certain communities and their leadership reflects those groups, including African Americans, Hispanic Americans, Asian or Pacific Islander Americans, Native American or Alaskan Native Americans, and Multi-racial Americans.[7] |

Credit Unions | Credit unions are not-for-profit organizations owned by their customers. Although like retail banks, they also have members that share a characteristic in common (e.g., where they live, their occupation, or an organization they belong to).[8] Credit unions may offer better terms to savers and borrowers because they aren’t as focused on profitability as the bigger banks.[9] |

Minority Depository Institutions (MDIs) | MDI is a formal federal designation for banks or credit unions that are either owned or directed primarily by African Americans, Asian Americans, Hispanic Americans, or Native Americans.[10] Minority depository institutions serve their communities by making a greater percentage of their home mortgage and small-business loans to minority and low-income borrowers than other financial institutions do.[11] There are 143 MDIs: Black or African American (20), Hispanic American (34), Asian or Pacific Islander American (71), Native American or Alaskan Native American (17) and Multiracial American (1).[12] |

Retail Banks | Retail banks include branches of national or multinational banks, smaller banks that have a local or regional presence, and online banks. Retail banks provide financial services including credit in the form of mortgages, auto loans, and credit cards; a safe place for people to deposit their money through savings accounts, certificates of deposit, and other financial products.[13] |

Kimbrough emphasizes the importance of relationship-building from the first meeting. Steve Zimmerman, Principal of Spectrum Nonprofit Services, describes the first steps of building a relationship as a “dance.”

Involve board members and tap your network. Board members and your network can help. Zimmerman suggests asking board members to identify people who might be receptive to building that relationship. Jessie-Black says, “It’s helpful to connect with other nonprofits that might already have a banking relationship.” Perhaps a foundation that supports your nonprofit can help facilitate the connection with a community bank.

Jessie-Black also recommends joining the local chamber of commerce: “Our community is small, and all things go through the chamber. That’s also where we get a chance to meet bankers that we typically don’t get to connect with otherwise.” She says that most chambers of commerce have a sliding scale membership fee for nonprofits.

Have a thorough picture of your finances. In the initial meeting, Jeremy Kohomban, President and CEO of The Children’s Village, suggests that nonprofit leaders should explain their accounts receivable and payables process. Depending on the nonprofit’s size, one person might handle both tasks. He says, “If that’s the case, bring that person to the meeting so that the banker is aware of your process to collect money. ”

Know your nonprofit’s needs. It’s important to be realistic about what your nonprofit needs. Kohomban stresses, “You need to know the line of credit number, and you don’t want to negotiate on that number.” He also says, “Banks can create something that meets your needs, if you make it clear and if they choose to. Don’t go into the search without clarity on what you need.”

Do your research. Elisabeth Risch, Assistant Director of the Metropolitan St. Louis Equal Housing and Opportunity Council, suggests reviewing the bank’s website to understand how it operates. For example, you might find out their structure, services offered to nonprofits (e.g., loans, investments, grants, and other tools), services available to the neighborhood you serve, and whether bank employees volunteer with nonprofits. Jesse Van Tol, President and CEO of the National Community Reinvestment Coalition, suggests looking at the bank’s Corporate Social Responsibility statement. “This fact-finding process allows you to learn where the community bank invests its funds and also gives you insight into how the bank wants to be perceived. For instance, is this a bank that wants to be seen as a leader in renewable energy, or helping innovative start-ups? Identifying the overlap between the services your nonprofit offers and the desired public image of the bank can be very helpful for creating or expanding relationships with funders.”

If the bank has a Community Economic Development Division or Community Reinvestment Act (CRA) Officer, Kimbrough says: “Meet with that person and let them know that you want to build a relationship with a bank that serves the people your nonprofit also serves.”

Learn about the bank’s history in the community. Historically, banks have played a significant role in upholding racist practices, including redlining.[14] Unfortunately, some continue to discriminate and maintain systemic racism.

Banks with a history of redlining may intentionally partner with under-resourced communities and nonprofits that serve them to address the injustice. Zimmerman gives an example of a nonprofit-community bank partnership, where the nonprofit provided financial literacy and job skills training to residents. The bank then offered financial services to those who completed the program. He adds, “This program prepared residents to sustain employment and manage their money, making it less risky to become the bank’s clients.” Through this type of partnership, both the nonprofit and bank accomplished their goals and expanded banking services to the community. More importantly, they provided resources and tools to empower residents to achieve and sustain better financial practices, which in turn, helps to improve their quality of life.

Learn more about the Community Reinvestment Act (CRA). Risch recommends nonprofit leaders sharpen their skills in CRA regulations. She says, “Banks get credit for CRA-related activities, including affordable housing, small business development, and services in low- and moderate-income communities. Nonprofit leaders need to know how they fit into those boxes.” Van Tol says, “This isn’t to say that banks only do CRA-eligible projects, but it is a significant motivator.”

Community Reinvestment ActWhat is it? In 1977, Congress passed CRA to encourage deposit-taking banks to reinvest in the communities where they operate. The federal law established CRA to combat redlining. CRA created a framework wherein community organizations, banking regulatory agencies, and financial institutions interact in assessing how well a financial institution is meeting the needs of under-invested communities.[15] How does it work? Federal agencies that regulate banks examine banks every two or three years for their CRA performance.[16] Banking regulators are required to consider comments from the public, including local organizations, in evaluating a bank’s CRA performance or in determining whether to approve an application for banks to merge or open new branches.[17] CRA doesn’t explicitly cover racial discrimination. However, the federal regulators can downgrade a CRA rating if they uncover evidence of illegal, abusive, or discriminatory lending on fair lending exams that occur approximately at the same time as CRA exams.[18] |

Shop around and test drive relationships. Some nonprofit leaders like Jessie-Black develop relationships with multiple banks to find the best fit. For example, her organization has a relationship with a local CDFI, although they don’t use its financial services or products. Zimmerman recommends test-driving the relationship before formalizing it or inviting bank representatives to join your board. For example, share your nonprofit’s financial situation and ask, “What might you recommend that we do?” See what the bank says and take it from there.

Make sure you leave meetings with a clear understanding of topics including:

What is the bank’s commitment to your mission? For Kohomban, his bank partner must understand his organization’s mission. If they don’t, it can be harder to explain, for example, why his organization is sometimes in the news when things go wrong. He says, “The Children’s Village, a 170-year-old organization, is not considered a sexy brand, but we do most of the most important and difficult work that must be done. We serve children and youth, some who have been in and out of jail and we speak publicly about the disproportionate impact of race. How Black and Brown children are locked up, placed in foster care, and separated from their families.” Kohomban emphasizes, “We need to build a relationship with a bank that’s proud to work with an organization, like ours, that takes risks to make the world a better place.”

What is the bank’s commitment to the local community? Kimbrough says, “All individuals should have access to reasonably priced capital,” meaning banks should make loans and other financial resources available to everyone.[19] He also points out, “Community banks [smaller in size that serve a local or regional area] care about communities and derive profits from purpose by investing capital in neighborhoods and businesses where it is most needed and the most productive, helping more people win and lift up generations.”[20]

Approximately 70 million Americans don’t have a bank account (unbanked) or access to traditional financial services (underbanked).[21] One in five Black Americans is unbanked.[22] Nearly half of Black households have limited access to retail banking services or none at all.[23] Black customers who have bank accounts pay more—$190 more for a checking account—compared with white customers.[24] When considering the communities your nonprofit serves, think about the poverty and homeownership rates. These factors are related to economic empowerment, and economic empowerment starts with banking.[25]

Kimbrough also suggests asking, “In what ways do you serve the population our nonprofit serves? How much credit is the bank issuing to that population?” This information may be hard to come by, but it will help determine if there are gaps in the credit needs of those you serve. In “David vs. Goliath: A Fight to Keep ‘Community’ in Banking,” Kimbrough describes community banks with a local or regional presence as the generator of self-sustaining financial ecosystems:

“At our bank [Midwest BankCentre], 95 cents of every local dollar on deposit stays in the local community, with statistics showing it will circulate at least six times throughout the regional economy. Those deposits support local people and businesses. Those people do business with other local employers. The community bank completes the cycle by issuing credit and making loans to people and businesses, keeping funds within the community.”

In Chicago, for every $1 banks (including various types of banks and non-bank mortgage companies) loaned in white neighborhoods, they invested 12 cents in the city’s Black neighborhoods and 13 cents in Latino areas.[26] Similarly, in Chicago, businesses in non-white communities received fewer business loans and smaller loan amounts than their counterparts in white communities.[27] These statistics support why Risch recommends these questions: “Are they giving grants and financially supporting nonprofits? Are they showing up at collaborative meetings or initiatives focused on the unbanked and underbanked? Are they offering financial education? Are they partnering with organizations providing financial education? Are they providing home loan mortgages in the neighborhoods where you operate and to the people you serve? Are they providing loans to small businesses and minority-owned businesses?” Ned Montgomery, board member of the United Way of Greater Philadelphia & Southern New Jersey and a former bank president, suggests asking your local community bank to provide financial advice to your nonprofit’s clientele.

Does the bank have an explicit and active commitment to racial equity? For Jessie-Black, racial equity and antiracism are primary factors in community bank partnerships. “What does their statement say? If they’re doing active work in the community, what is it? Is that bank forward-thinking and looking at their corporate structure and how many people of color are in high-ranking positions and serving on their board of directors?” Kimbrough asks, “Does the bank have representation from the entire service area?”

Risch and her CRA advocacy coalition have always asked banks about addressing disparities impacting Black and Latinx borrowers and communities. But, she says, “Recently, we started asking more questions after the murder of Mr. George Floyd about banks’ Diversity, Equity, and Inclusion statements.” The group also conducts an annual survey that asks: Are they making statements about racial equity? Are they making relevant commitments? Are they tracking those commitments? What else are they doing in the racial equity space?

Kohomban says, “On this question of equity and social justice change, leadership matters. If you really want to do something, you have to bring money, effort, and take risks. Banks aren’t big risk-takers. Not beyond the performative, which is easy.”

BlueHub Capital, a national CDFI that lends over $100,000,000 annually to projects that serve low-income communities, and predominantly communities of color, conducts a rigorous impact screen for every project it finances. Projects must meet BlueHub standards for both credit and impact. Among other things, BlueHub’s impact screen assesses the extent to which local community members have agency over projects, how extensively projects support BIPOC borrowers and clients, and projects’ track-record for generating positive outcomes for economically disadvantaged community members, and particularly for community members of color. BlueHub finances a range of facilities projects, including education, affordable housing, community health centers.[28]

BlueHub Capital is a founding member of a collaboration of CDFIs focused on racial equity in education.[29] The collaboration intentionally engaged Black educators who were educating funders about how to assess educational projects’ ability to effectively support BIPOC children, families, and communities. Catherine Dun Rappaport, Vice President of Learning and Impact Measurement at BlueHub Capital, says, “My colleagues and I needed to learn from people who were walking the walk in a way that we couldn’t understand.” Through the partnership, BlueHub created questions to ensure the public charter school projects they finance intentionally and effectively support students of color, e.g., by using culturally responsive pedagogy, employing significant numbers of BIPOC educators and leaders, not over-suspending students of color, and creating environments that welcome and celebrate BIPOC families.

Does the bank understand nonprofit finances? Zimmerman asserts that your nonprofit and community bank must have a mutual understanding of finances. He says, “Just because a banker knows finance doesn’t mean they understand nonprofit finance.” This issue is critical in establishing a banking relationship. Nonprofits shouldn’t move forward if the banker and the bank aren’t proficient in nonprofit finance.

For Kohomban, his community banker must understand his organization’s funding streams. He says, “We need a bank that understands how government contracts process payments to nonprofits. If your business plan includes government contracts, donors, and pledges, explain pledge collection, your event cycle, and your margins. Most good human services nonprofits work within slim margins.”

What services does the bank offer? Polanco points out that if a nonprofit serves a historically under-invested neighborhood, there’s a chance that its financials and balance sheets might not be as strong as other organizations, making it difficult to obtain credit. Polanco acknowledges the high credit standards of large commercial banks and hopes that community banks will be open to exploring the benefits of working with nonprofits and take time to understand their business model. Smaller balance sheets don’t necessarily translate into an inability to repay.

She also says, “Nonprofits should question how the community bank ensures it offers competitive services. For example, your community bank should be a holistic business partner offering a technology platform that will help strengthen internal controls and reduce risk for both the customer and the bank.” Kimbrough argues, “Community banks not only offer the same modern, online services that big banks do, but they also do so at a lower cost.”[30]

Does the bank offer anything beyond financial services? Montgomery says, “The relationship between a nonprofit and a community bank can’t solely be about money.” For example, bank employees have been a good source of volunteers for the United Way of Greater Philadelphia & Southern New Jersey’s VITA (Volunteer Income Tax Assistance) program which offers free tax preparation and financial counseling services to low- and moderate-income taxpayers.[31] He suggests asking, “What about the bank staff volunteering, providing expertise to your nonprofit CFO, or offering leadership training or guidance on raising money? Could the bank staff provide sales training to your development staff?”

Kohomban ensures that his community bank “has the bench strength” to build his nonprofit’s capacity. He explains, “We don’t have extra staff in the Finance Office trained on the latest and greatest technology. I want a bank that can invest in my team by sharing the best technology and tools.” Kohomban makes it clear to the bank’s president that he wants access to all benefits.

What services does the bank offer to your employees? Jessie-Black inquires about bank services for her organization’s employees. She says, “We also have relationships with some credit unions for the benefit of employees, even though we don’t have any deposits with them.” She also points out, “We deal with marginalized communities in the nonprofit sector. Some individuals don’t see the importance of having an account at a bank or can’t get an account. So, we press banks not to charge fees to cash their checks.”

What is a mutually beneficial relationship? Kimbrough says, “Manage your expectations with your local community bank. It’s unrealistic to think that banks have an unlimited amount of money for charitable gifts. Otherwise, they compromise their sustainability.” As a nonprofit, you want to bring something to the relationship because the bank wants a return on its investment. Polanco asks, “Are you as a nonprofit willing to invest some of your dollars into your local community bank rather than investing them with the larger banks?”

You might emphasize the impact your nonprofit has on the community. For example, Jessie-Black tells bankers, “In North Carolina, nonprofits represent one out of every 10 jobs. We contribute to the economic viability of the state.” Information like this highlights the nonprofit’s important role in the economy and positions it as an asset worthy of investment.

Kohomban recounts his biggest lesson learned in working with a bank: “Have clarity around the transactional relationship with a bank—here is what I need, what I bring, and what I think you can offer. When there’s clarity on those three big points, you have a solid transactional relationship that is mutually beneficial.”

Kimbrough suggests asking how the bank maintains relationships: “Are we assigned a bank officer? Is the leadership of the bank accessible?” He also recommends finding out if the bank has an advisory board which may be an opportunity for your nonprofit to provide insight into how the bank can meet the community’s financial needs.

Kohomban says that having a relationship at the highest level is the most important factor in working with his community bank. He says, “I’m a phone call away from the bank’s president. Regardless of size, nonprofits need to be highly valued customers of banks. We do important work in our communities.” Zimmerman advises, “You want to have an open, honest, transparent relationship with your bank. You want to be frank about your experience and how things are going.”

Continually assess the bank’s commitment to your values. Jessie-Black holds her community banks accountable by ensuring they’re not harming community members who either work for nonprofits or engage in their services. Also, she examines who’s in charge of the smaller bank or branch location she partners with and questions what their equity plan looks like for their executive teams and the community’s upward mobility.

Jessie-Black also acknowledges that it can be challenging to hold banks accountable. But, she says, “If you don’t feel valued as you try to build a relationship with the bank in which you hold your funds, moving on to another bank is always appropriate. We’ve done that several times over the 17 years I’ve been a part of the organization.”

Share your financial story. Zimmerman highlights, “We can only have community impact if we have the capital to deliver on it. A nonprofit’s financial story includes saying, ‘Our funding comes from X foundation or individual and is capitalized through X bank.’ There’s also a piece to say, ‘We could grow if we increase our capital.’ So, talk about who gave you capital and who didn’t give you capital. Don’t be afraid to state the facts. For example, this company didn’t support us. This bank did.”

Monitor CRA in your community. Van Tol points out, “Banks have this affirmative obligation to serve the community, under the Community Reinvestment Act (CRA). So, it’s a powerful accountability mechanism. But, of course, sometimes banks don’t like that because it could be negative.”

There’s also the case where nonprofits can use CRA positively to highlight where one bank does a better job than another. Risch says, “Community groups, including nonprofits, should be the ones providing input into how the bank has met the community’s credit needs or not. The problem is that it’s confusing to figure out exactly how to do this through CRA. So, that’s where connecting with a community-based organization that understands CRA or with the National Community Reinvestment Coalition can be helpful.”

Choosing a community bank is important. Kimbrough says, “Nonprofits should invest their money in banks that are not insulated from the community’s challenges.” Your nonprofit can be instrumental in helping your community bank to meet neighborhood needs through financial support, products, and services. So, build a relationship with a community bank that supports your nonprofit’s mission and the community you serve. Furthermore, that banking relationship might come in handy in times of emergency. Be sure to determine the community bank or banks that works best for your nonprofit, do the prep work before meeting with a banker, be ready to ask the questions important to you, maybe test drive the relationship, make the decision, then grow the relationship. Zimmerman says, “There’s a lot of strength in that relationship. If we’re intentional and invest the time, we can find a way to make both of us stronger, ultimately making the community stronger.” Perhaps more nonprofit-community bank relationships can move from transactional to transformational, and we can partner to fight injustice.

CDFIs and banks share a market-based approach to serving communities and partner to develop innovative ways to deliver loans, investments, and financial services to distressed communities.[32] Dana Britto, Managing Director at BDO FMA, describes the Arts and Culture Loan Fund: “It started in 2009 largely in response to the recession, when smaller organizations, especially arts organizations, weren’t able to access credit from traditional financial institutions. The Fund provides access to capital and limited technical assistance and capacity-building support. However, through an evaluation of the program after its first five years, nonprofit participants shared that they needed more rigorous support on the technical assistance and capacity building end, which led to BDO FMA joining the partnership.”

The partnership includes the MacArthur Foundation, a funder; IFF, formerly Illinois Facilities Fund, a CDFI that serves as the overall program manager and a participating lender; BDO FMA, financial management service provider; and Fifth Third Bank, a participating lender.[33] Britto explains, “MacArthur has specific agreements with IFF and Fifth Third Bank that set up the terms around the Program Related Investment that funds the loan guarantee.[34] We were able to make loans more accessible to organizations that traditionally wouldn’t be able to access them because they’re almost or completely fully backed by the guarantee from MacArthur. So, if an organization can’t fully repay, the participating lenders can draw from the MacArthur guarantee.” Kevin Iega Jeff, Co-Founder & Executive/Artistic Director of Deeply Rooted Dance Theater, says “The Fund really focuses on educating organizations, so they understand what banks are looking for. In our case, we received a line of credit to better manage our cash flow throughout the year. That’s major. The advice I would give to nonprofits is take advantage of this opportunity. In doing so, you can foster an organic relationship with finance sooner than later.[35]

Dun Rappaport says, “As a CDFI, we are more creative and flexible than conventional lenders. We structure our deals with terms that align specifically with our borrowers’ needs and capital flows, eliminate requirements that hamstring borrowers’ ability to run programs, and provide early-stage lending that’s essential, but that banks won’t typically provide, or won’t provide at the level needed. We also ‘go deep,’ forging deep relationships with local communities and lending for a range of critical projects: affordable housing, schools, healthcare, you name it!”

For example, she highlights how, in 2017, BlueHub Capital began working in Frayser, an extremely high-poverty community in Memphis, to finance a high performing, Black-led charter school that serves higher percentages of low-income and Black students than local schools. BlueHub built on that effort by partnering with The Works, a BIPOC-led and serving nonprofit community development corporation, to create affordable housing in the same area. BlueHub made a $2.6 million loan to The Works to support the redevelopment of 146 units of affordable housing. BlueHub continues to partner with community leaders in and near Frayser to finance projects that provide essential goods and services. Since 2017, BlueHub has invested close to $40,000,000 in housing, schools, and other facilities projects in low-income Memphis neighborhoods.

Leap Ambassadors Community support team member Samantha Sherrod served as lead author, with contributions from Dana Britto, Catherine Dun Rappaport, Kevin Iega Jeff, Barbara Jessie-Black, Orv Kimbrough, Jeremy Kohomban, Ned Montgomery, Hilda Polanco, Elisabeth Risch, Jesse Van Tol, and Steve Zimmerman.

[1] William P. Ryan, “Nonprofit Capital: A Review of Problems and Strategies,” (2001), 1.

[2] Mehrsa Baradan, The Color of Money: Black Banks and the Racial Wealth Gap (2017), 260-261: Most Black neighborhoods are “banking deserts,” neighborhoods abandoned by mainstream banks, which are regulated and heavily subsidized in the U.S. and have historically discriminated against Black people.

[3] Minority Depository Institutions Program

[4] Local Initiatives Support Corporation

[5] Ibid.

[6] CDFI Coalition: About CDFIs

[7] Mighty Deposits Guide, 2021 Edition, CDFIs: What They Are and How to Bank with One.

[8] Justin Pritchard and Khadija Khartit, “Get Up to Speed on the Different Types of Banks,” The Balance, January 22, 2022.

[9] Kimberly Amadeo and Eric Estevez, “Retail Banking, It’s Types and Economic Impact,” The Balance, November 29, 2020.

[10] Greg Daugherty, “Minority Depository Institution (MDI),” Investopedia, July 30, 2020.

[11] Ibid.

[12] Ibid.

[13] Kimberly Amadeo and Eric Estevez, “Retail Banking, It’s Types and Economic Impact,” The Balance, November 29, 2020.

[14] Mehrsa Baradan, The Color of Money: Black Banks and the Racial Wealth Gap (2017), 105-6: In the 1930s, the Home Owners Loan Corporation mapped out metropolitan regions and neighborhoods based on race to determine their level of desirability. Green neighborhoods were homogeneous and white. At the other end of the scale, the red neighborhoods were predominantly Black. Race was a greater factor in a neighborhood’s predicted decline than other structural characteristics such as the age of homes, proximity to city centers, creditworthiness of residents, transportation opportunities, public parks, and other features. Redlining was used to institutionalize racial segregation in housing and made it a formal feature in banks determining mortgage lending.

[15] National Community Reinvestment Coalition, CRA 101 Manual.

[16] Finely Coyl, Anti-Eviction Mapping Project, and California Reinvestment Coalition, “Community Reinvestment Act.”

[17] National Community Reinvestment Coalition, CRA 101 Manual.

[19] Rising Together: Midwest BankCentre’s 2020 Community Impact Report

[20] Kimbrough, Orvin T., “David vs. Goliath: A Fight to Keep ‘Community’ in Banking.”

[21] Mehrsa Baradan, How the Other Half Banks: Exclusion, Exploitation, and the Threat to Democracy (2015), 139.

[22] Ward Williams, “Black-Owned Banks by State,” Investopedia, January 27, 2022.

[23] Angela Glover Blackwell and Michael McAfee, “Banks Should Face History and Pay Reparations,” The New York Times, June 26, 2020.

[24] Ibid.

[25] Ward Williams, “Black-Owned Banks by State,” Investopedia, January 27, 2022.

[26] Linda Lutton, Andrew Fan, and Alden Loury, “Where Banks Don’t Lend,” WBEZ91.5Chicago, June 3, 2020.

[27]Alden Loury, “Lower-Income, Minority Areas in Chicago Region Losing Out on Millions in Small Business Loans,” WBEZChicago, August 7, 2019.

[28] BlueHub Capital: Community Development Financing – How We Work

[29] CDFI Racial Equity Collaborative on Education is spearheaded by Self-Help and its memberships consists of BlueHub Capital, Capital Impact Partners, IFF, Nonprofit Finance Fund, LISC, and Low Income Investment Fund.

[30] Kimbrough, Orvin T., “David vs. Goliath: A Fight to Keep ‘Community’ in Banking.”

[31] United Way of Greater Philadelphia and Southern New Jersey Volunteer Income Tax Assistance program.

[32] CDFI Coalition: About CDFIs

[33] MacArthur Foundation Arts & Culture Loan Fund Grant Guidelines

[34] Paul Brest, “Investing for Impact with Program-Related Investments,” Stanford Social Innovation Review, Summer 2016.

[35] MacArthur Foundation Arts and Culture Loan Fund (iff.org)

The Leap of Reason Ambassadors Community is a private community of experts and leaders who believe that mission and performance are inextricably linked. Our resources are collaboratively developed and offered to the field to support organizations on their journeys to high performance.

We use cookies for a number of reasons, such as keeping our site reliable and secure, personalising content and providing social media features and to analyse how our site is used.

Accept & Continue